(11) 95720-0227

8 20: Contribution Margin Ratio Business LibreTexts

Each profit measure can be expressed as total dollars or as a ratio that is a percentage of the total amount of revenue. The contribution margin represents how much revenue remains after all variable costs have been paid. It is the amount of income available for contributing to fixed costs and profit and is the foundation of a company’s break-even analysis. In our example, the sales revenue from one shirt is \(\$15\) and the variable cost of one shirt is \(\$10\), so the individual contribution margin is \(\$5\). This \(\$5\) contribution margin is assumed to first cover fixed costs first and then realized as profit.

Contribution Margin Calculator

Let’s examine how all three approaches convey the same financial performance, although represented somewhat differently. However, this implies that a company has zero variable costs, which is not realistic for most industries. As such, companies should aim to have the highest contribution margin ratio possible, as this gives them a higher likelihood of covering its fixed costs with the money remaining to reach profitability.

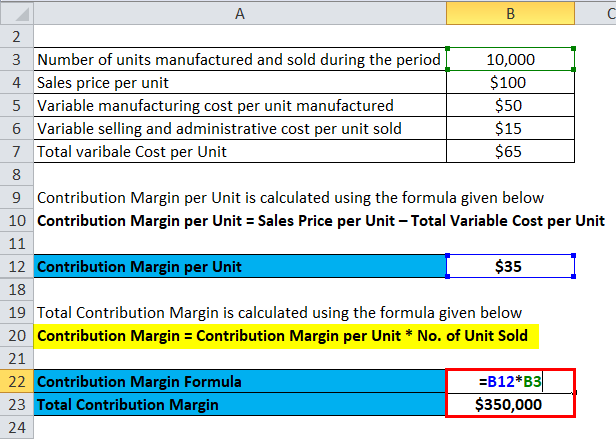

Contribution Margin Formula Components

On the other hand, contribution margin refers to the difference between revenue and variable costs. At the same time, both measures help analyze a company’s financial performance. However, an ideal contribution margin analysis will cover both fixed and variable cost and help the business calculate the breakeven. A high margin means the profit portion remaining in the business is more.

What is the difference between the contribution margin ratio and contribution margin per unit?

In short, it is the proportion of revenue left over after paying for variable costs. The first step to calculate the contribution margin is to determine the net sales of your business. Net sales refer to the total revenue your business generates as a result of selling its goods or services. That is, fixed costs remain unaffected even if there is no production during a particular period. Fixed costs are used in the break even analysis to determine the price and the level of production. Yes, the Contribution Margin Ratio is a useful measure of profitability as it indicates how much each sale contributes to covering fixed costs and producing profits.

- A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation.

- The CM ratio is extremely useful since it shows how the contribution margin will be affected by a change in total sales.

- The ratio can help businesses choose a pricing strategy that makes sure sales cover variable costs, with enough left over to contribute to both fixed expenses and profits.

- But what is considered “good” largely can depend on your industry.

- Say a company could make three different products on one machine.

- You can calculate the contribution margin by subtracting the direct variable costs from the sales revenue.

Contribution Margin Ratio (CM

Thus, here we use the contribution margin equation to find the value. When there’s no way we can know the net sales, we can use the above formula to determine how to calculate the contribution margin. Here, we are calculating the contribution margin on a per-unit basis, but the same values would be obtained if we had used the total figures instead. We’ll next calculate the contribution margin and CM ratio in each of the projected periods in the final step. Thus, it will help you to evaluate your past performance and forecast your future profitability.

Regardless of how much it is used and how many units are sold, its cost remains the same. However, these fixed costs become a smaller percentage of each unit’s cost as the number of units sold irs hours of operation increases. The concept of this equation relies on the difference between fixed and variable costs. Fixed costs are production costs that remain the same as production efforts increase.

To demonstrate this principle, let’s consider the costs and revenues of Hicks Manufacturing, a small company that manufactures and sells birdbaths to specialty retailers. The contribution margin ratio refers to the difference between your sales and variable expenses expressed as a percentage. That is, this ratio calculates the percentage of the contribution margin compared to your company’s net sales.

If total fixed cost is $466,000, the selling price per unit is $8.00, and the variable cost per unit is $4.95, then the contribution margin per unit is $3.05. The break-even point in units is calculated as $466,000 divided by $3.05, which equals a breakeven point in units of 152,787 units. Using this metric, the company can interpret how one specific product or service affects the profit margin. The fixed cost like rent of the premises, salary, wages of laborers, etc will remain the same irrespective of changes in production.